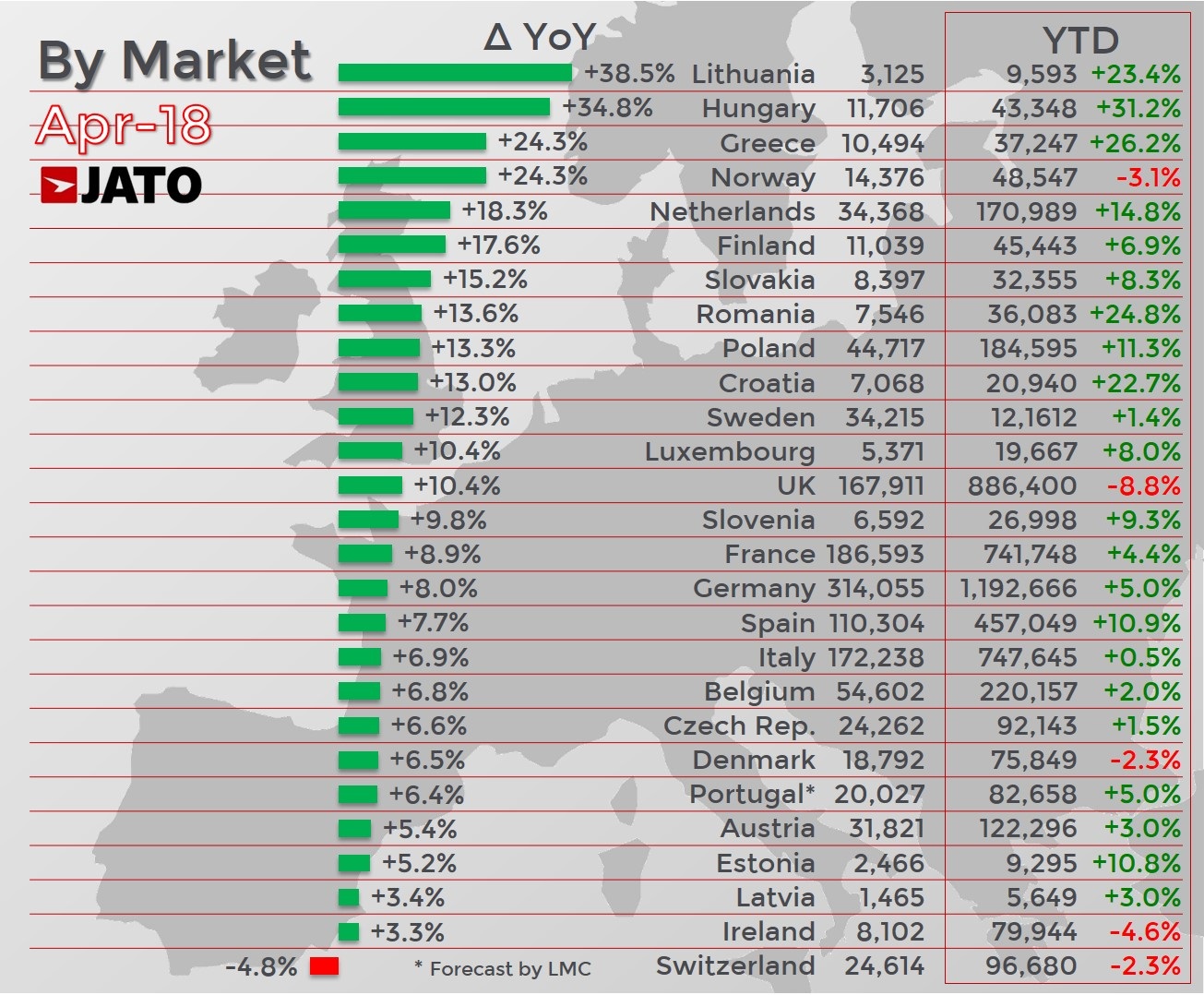

The European car market recorded its best April performance since 2008, with volume up by 9.0% as 1.34 million cars were registered, signifying that the industry has recovered strongly from the 5.2% decline it posted in March 2018. This was the highest monthly increase since March 2017 and boosts the year to date figures to 5,607,856 registrations – an increase of 2.5% year on year.

Switzerland was the only market to register a decline, whilst Germany recorded 314,055 registrations – boosted by the demand for SUVs, which were up 23% due to the strong performance of the Volkswagen T-Roc and Ford Kuga. The Italian market appeared to be unaffected by political uncertainty as more private registrations increased overall results.

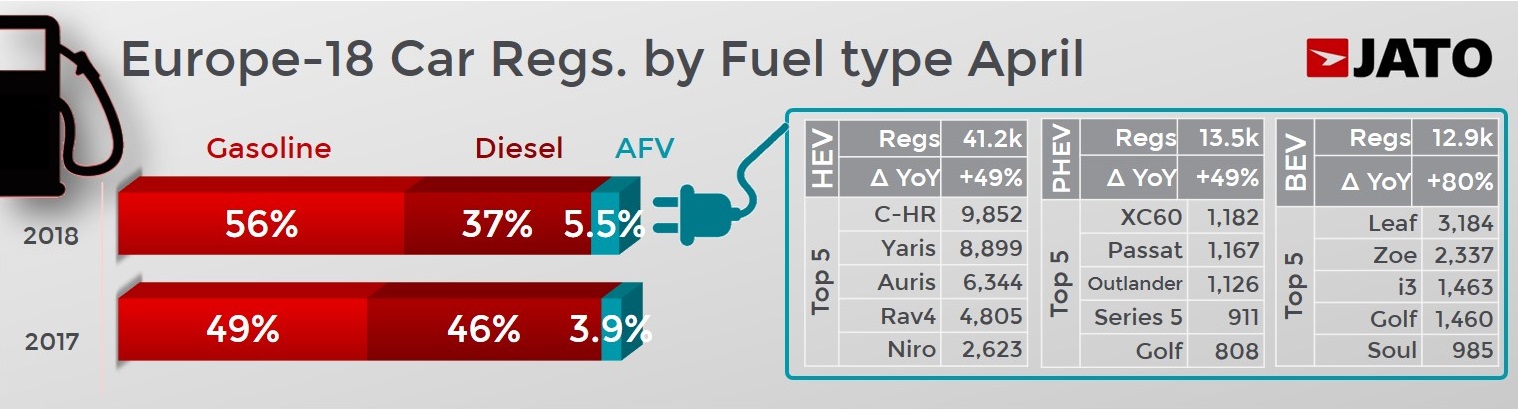

Results from 18 markets show that diesel registrations continued to fall in April, with volume down by 13.2% to 453,500 units – a market share of 36.7%. Meanwhile, diesel losses continued to be gasoline’s gain, as strong demand increased their volume by 25% to 692,300 units – a market share of 56.1%. Alternative Fuelled Vehicles continued to gain traction, with volume also up by 53.5% as they counted for 5.5% of total registrations. Among them there were 41,200 hybrid, 13,500 plug-in and 13,000 fully-electric registrations.

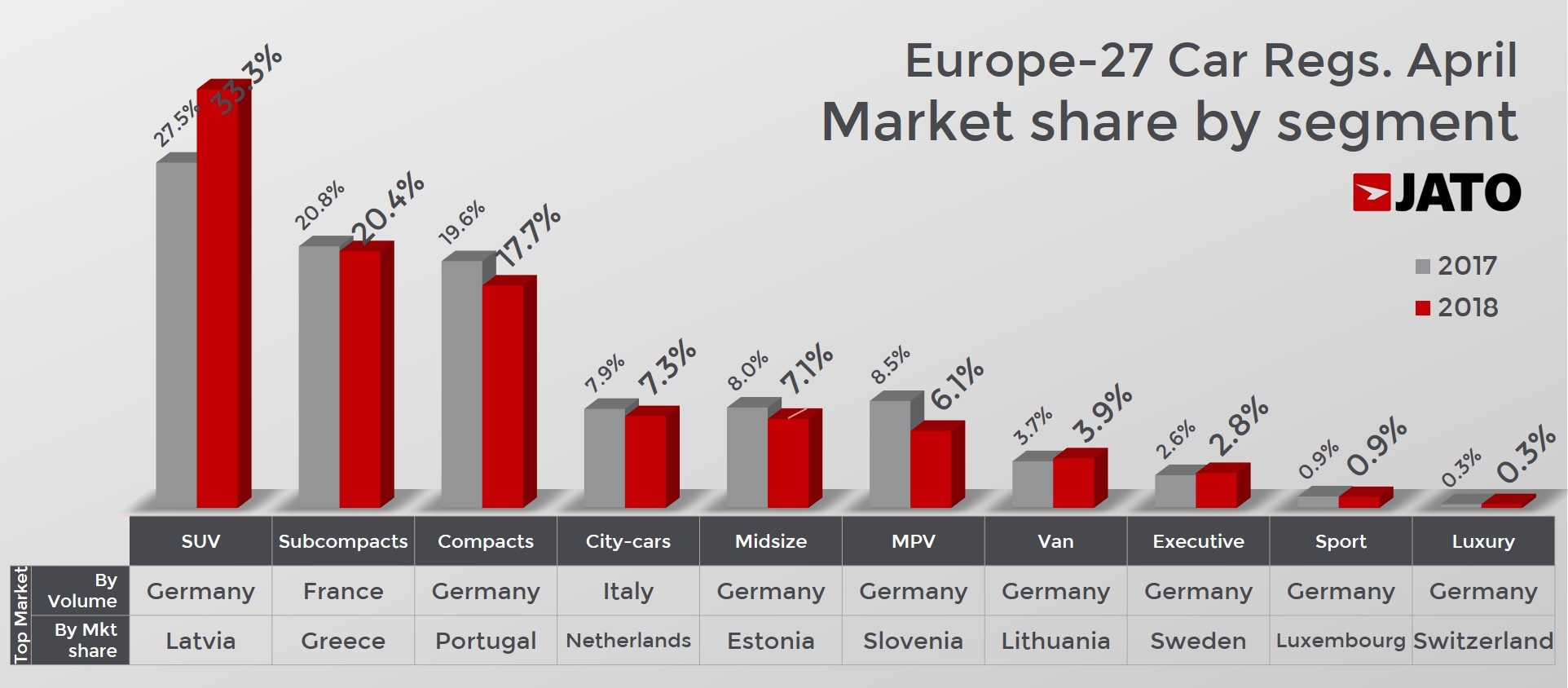

Small SUVs were the biggest driver of growth in the segment, with 166,700 registrations. Their volume was up by 45% as they were boosted by new arrivals like the Volkswagen T-Roc, Dacia Duster, Citroen C3 Aircross, Opel Crossland, Seat Arona, Kia Stonic and Hyundai Kona. Compact SUV’s volume increased by 27%, which equates to 40,000 more units than in April 2017. They remain the top-selling type of SUV in Europe, and their April volume was boosted by double-digit growth by the Peugeot 3008, Ford Kuga, Toyota C-HR, as well as new arrivals like the Skoda Karoq, Jeep Compass and Opel Grandland.

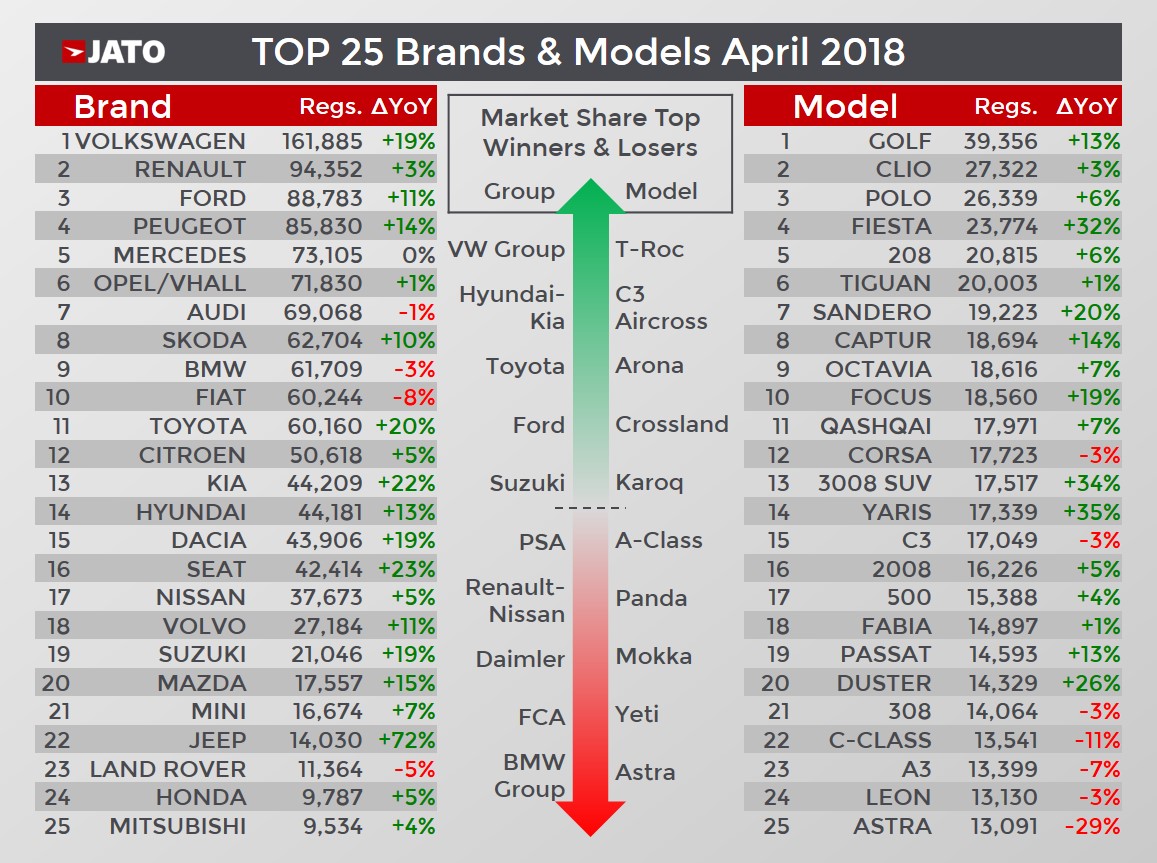

For the second consecutive month, Volkswagen Group gained the most market share across Europe, jumping from 24.9% in April 2017 to 25.7% in April 2018. This was due to the strong performances of Skoda, Seat and the Volkswagen brand. SUVs counted for 26% of the group’s registrations, more than any other segment.

Hyundai-Kia posted the second largest market share gain, as its volume grew by 17.4% to 88,400 units. It was the sixth largest car maker in April, however there was only a marginal gap between them and FCA, who recorded 89,100 units and came in fourth place. Toyota also performed well in terms of market share gain due to the strong performance of its hybrid range.

Premium car makers like the BMW Group and Daimler lost ground as a result of double-digit falls in their midsize and compact models. Their market share also suffered as a result of minimal growth in the premium car segment, which increased by only 1.7% in April to 297,800 units.

Other models that performed well in April include the Ford Fiesta, Dacia Sandero, Renault Captur, Ford Focus, Peugeot 3008 and Toyota Yaris. Further down the rankings, the Toyota C-HR, Mercedes GLC, BMW 5-Series, Ford Ecosport and Renault Scenic also posted good months and increased their volume.

Among the market’s newest launches, the Citroen C3 Aircross was the 45th best-selling car in Europe, whilst the Opel Crossland and Seat Arona came 53rd and 54th, respectively. Meanwhile, the Opel Grandland came 77th, the Kia Stonic came 94th and the Hyundai Kona came 99th.

Other recent launches include the new Volvo XC40 with 3,316 units, Jaguar E-Pace with 2,513 units, BMW X2 with 2,272 units, Range Rover Velar with 2,122 units, and the DS 7 Crossback with 1,576 units.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}